6 Proven Ways to Simplify Your Personal Finances and Reduce Financial Stress

Financial complexity is one of the most underrated sources of chronic stress in modern life. When your money is scattered across multiple accounts, buried under confusing subscriptions, and constantly demanding your attention, it drains mental energy even when you are not actively thinking about it. The research confirms what many people feel but rarely name: financial stress is pervasive, persistent, and deeply damaging to health, relationships, and decision-making. The good news is that simplifying your personal finances does not require a financial degree or a dramatic overhaul — it requires a handful of deliberate, evidence-backed changes that you can begin this week.

Why Financial Complexity Creates So Much Hidden Stress

According to the American Psychological Association, money is the single leading cause of stress for American adults, with 65% of Americans reporting money-related stress and one in four experiencing it most or all of the time. A significant driver is complexity itself — the mental burden of tracking multiple accounts, managing irregular payments, and making constant micro-decisions about money. Psychologists call this pattern financial avoidance: the tendency to delay financial tasks because thinking about money triggers anxiety. Paradoxically, avoidance makes stress worse, because underlying problems compound while attention is turned away.

The National Institutes of Health has found that people with greater financial wellbeing are not just richer — they are less stressed, more motivated, have better family relationships, and report better physical and mental health [1]. Simplifying your finances is not just a money strategy. It is a health strategy.

[1]

Way 1 — Automate the Essentials and Remove Willpower from the Equation

What to Automate First

The most impactful first step in financial simplification is to automate every recurring financial obligation and saving goal. When money moves automatically, you eliminate the need to make the same decisions repeatedly and remove the risk of forgetting or redirecting funds under stress. Here is a simple process to get started:

- List every recurring bill and payment obligation, including annual ones

- Set each bill to autopay from a dedicated checking account on a fixed date

- Set a recurring transfer from checking to savings for a fixed amount on payday

- Set a recurring contribution to your retirement or investment account if applicable

- Review automated payments quarterly to catch changes or unused subscriptions

The Behavioral Science Behind Automation

Behavioral economists have established that reducing friction in financial decisions leads to dramatically better outcomes. When saving requires a deliberate action, people consistently underprioritize it. When saving happens automatically, it becomes the default — and defaults are extraordinarily powerful in shaping behavior. Automating your finances saves an estimated 10 or more hours per month in financial task management and eliminates late fees entirely.

Way 2 — Consolidate Your Accounts to Reduce Mental Load

The Hidden Cost of Too Many Accounts

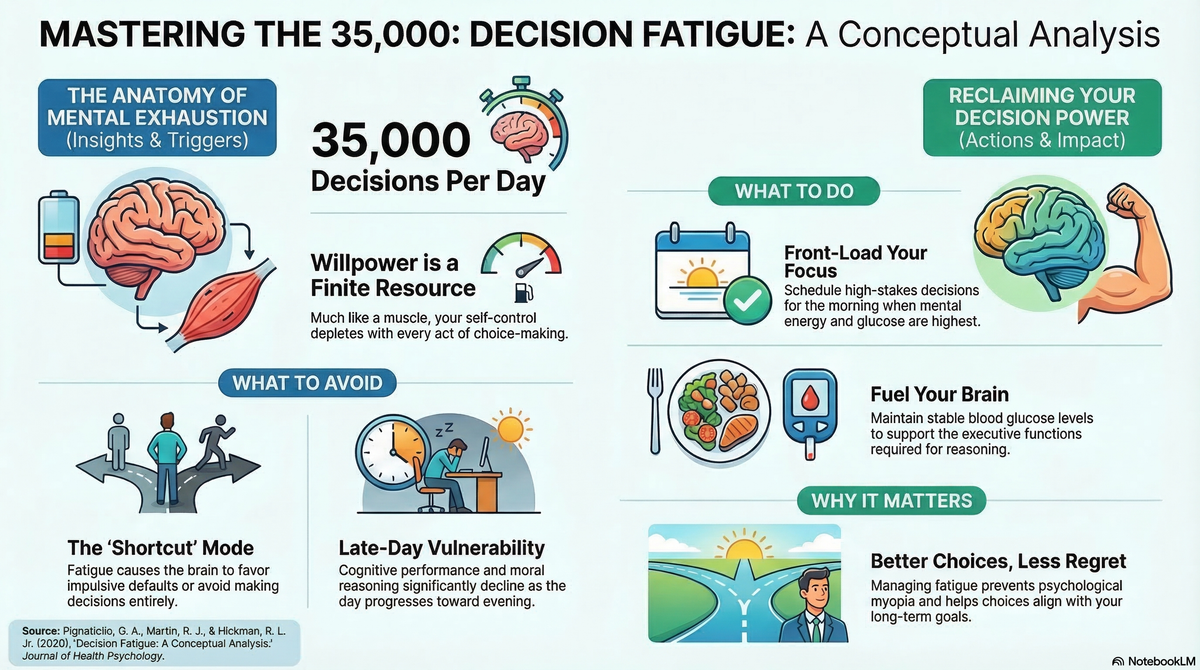

Many people accumulate financial accounts gradually through individually sensible decisions that add up to an unwieldy whole. Research on decision fatigue shows that each additional decision degrades the quality of subsequent ones. Every extra account in your financial life is an additional tax on your cognitive bandwidth [2]. A streamlined structure — one primary checking account, one high-yield savings account, and one investment account — radically reduces administrative friction.

[2]

How to Consolidate Effectively

Start by listing every financial account you currently hold. Identify any that are redundant, inactive, or no longer serving a clear purpose. Key candidates for consolidating bank accounts include:

- Duplicate savings accounts with no specific purpose

- Old accounts at banks you no longer actively use

- Multiple credit cards with overlapping rewards categories

- Unused investment accounts with small balances that incur fees

Keep accounts that serve a distinct, ongoing purpose — such as a dedicated emergency fund account, a joint account for shared household expenses, or a Health Savings Account with tax advantages.

Way 3 — Adopt a Simple, Sustainable Budgeting Framework

The 50/30/20 Rule: Simplicity as a Feature

One reason people abandon budgets is that they are too detailed and therefore too fragile. The 50/30/20 budgeting rule replaces hundreds of line-item decisions with a single three-bucket framework: 50% of after-tax income to needs (housing, food, transportation, insurance), 30% to wants (dining, entertainment, travel), and 20% to savings and debt repayment [3]. This framework does not require tracking every purchase. It requires only that you know roughly what your total spending in each category looks like each month.

[3]

Adapting the Framework to Your Reality

In high-cost-of-living cities, 50% for needs may not be achievable. Adjust to 60% needs, 20% wants, 20% savings — and focus on gradually reducing the needs percentage through strategic choices over time. Apps like YNAB or a simple spreadsheet can help you implement the framework with minimal ongoing effort.

Way 4 — Build a Financial Cushion That Absorbs Shocks

The Emergency Fund: Your Biggest Financial Stress Reducer

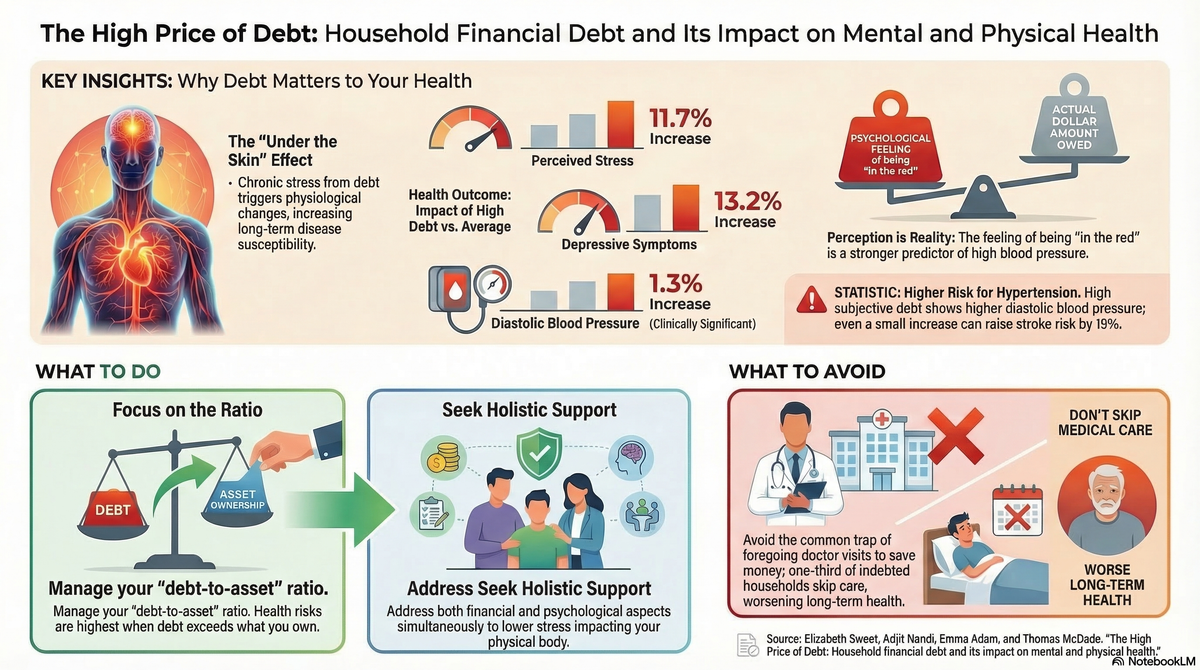

No single financial habit does more to reduce financial anxiety than maintaining an adequate emergency fund [4]. Financial planners consistently recommend holding three to six months of essential living expenses in a liquid, easily accessible savings account — separate from your regular checking account. Research on financial stress is unambiguous: a cash cushion dramatically reduces the psychological impact of financial surprises, from a car repair to a job loss. The fund does not need to earn high returns; its purpose is insurance against the chaos that derails most financial plans.

[4]

Building One When You Feel Like You Have Nothing Left

The most common obstacle is the feeling that nothing is left over after expenses. The solution: start embarrassingly small and automate it immediately. Here are the steps to build an emergency fund from zero:

- Open a separate savings account specifically labeled for emergencies

- Set an initial target of $500 to $1,000 as your first milestone

- Automate a fixed weekly or monthly transfer, however small

- Direct windfalls like tax refunds or bonuses to the fund until fully funded

- Treat the account as inaccessible except for genuine emergencies

Way 5 — Schedule a Monthly Money Date

What a Money Date Is and Why It Works

A money date is a scheduled, low-pressure monthly ritual for reviewing your finances. Georgetown University and America Saves research found that simply having a financial plan makes you twice as likely to achieve your goals. A monthly money date is the mechanism that keeps that plan alive and responsive to your actual life. By making financial review a regular, low-stakes ritual rather than a crisis response, you build a relationship with your money characterized by awareness and agency rather than dread and avoidance.

What to Cover in 15 Minutes

A monthly money date does not need to be exhaustive. A focused five-item agenda keeps it sustainable:

- Review total spending for the month against your budget framework

- Check savings account balances and confirm automated transfers are working

- Note any upcoming large expenses and adjust next month's plan accordingly

- Review any new subscriptions or recurring charges and cancel unused ones

- Celebrate one financial win from the month, however small

For couples, the money date serves an additional function: it keeps both partners aligned on shared goals and reduces the financial misalignment that is one of the leading causes of relationship conflict. Couples who discuss finances regularly report fewer money-related arguments and greater relationship satisfaction.

Way 6 — Simplify Your Debt Strategy

Choosing a Payoff Method That Matches Your Psychology

The two most researched debt payoff approaches are the debt avalanche (paying highest-interest debt first, minimizing total interest paid) and the debt snowball (paying smallest balance first, generating psychological momentum). Research shows the snowball method produces better real-world results for many people because motivation and consistency matter more than mathematical optimality. Choose the method that you will actually stick with.

Consolidating Debt Payments to Reduce Complexity

If you are managing payments to multiple creditors, debt consolidation — rolling several debts into a single loan with one monthly payment — dramatically reduces cognitive load. Balance transfer credit cards and personal consolidation loans are the most common vehicles. The goal is not just to reduce interest costs; it is to simplify your financial picture: one payment, one due date, one interest rate to track.

The Psychological Payoff of Financial Simplicity

Research on physical decluttering shows that clearing your living space reduces cortisol and improves mood, focus, and personal agency. The same principle applies to your finances. When you simplify your money — fewer accounts, automated systems, clear frameworks, and regular reviews — you reclaim mental bandwidth that was consumed by low-grade financial worry. The NIH research on financial wellbeing makes clear that this is not just about money: people with simplified, well-organized finances report better relationships, stronger motivation, and measurably better physical and mental health.

Financial simplicity is not a sacrifice. It is a compounding investment in every dimension of your wellbeing. You do not need to implement all six strategies at once. Pick one — automate your savings, schedule your first money date, or close one unused account — and build momentum from there. The best financial system is the one simple enough that you will actually use it.

References

-

Sweet, E., Nandi, A., Adam, E. K., & McDade, T. W.

The high price of debt: Household financial debt and its impact on mental and physical health.

Social Science & Medicine, 2014 91, 94–100 -

Pignatiello, G. A., Martin, R. J., & Hickman, R. L. Jr. Decision fatigue: A conceptual analysis.

Journal of Health Psychology, 2020 25(1), 123–135

-

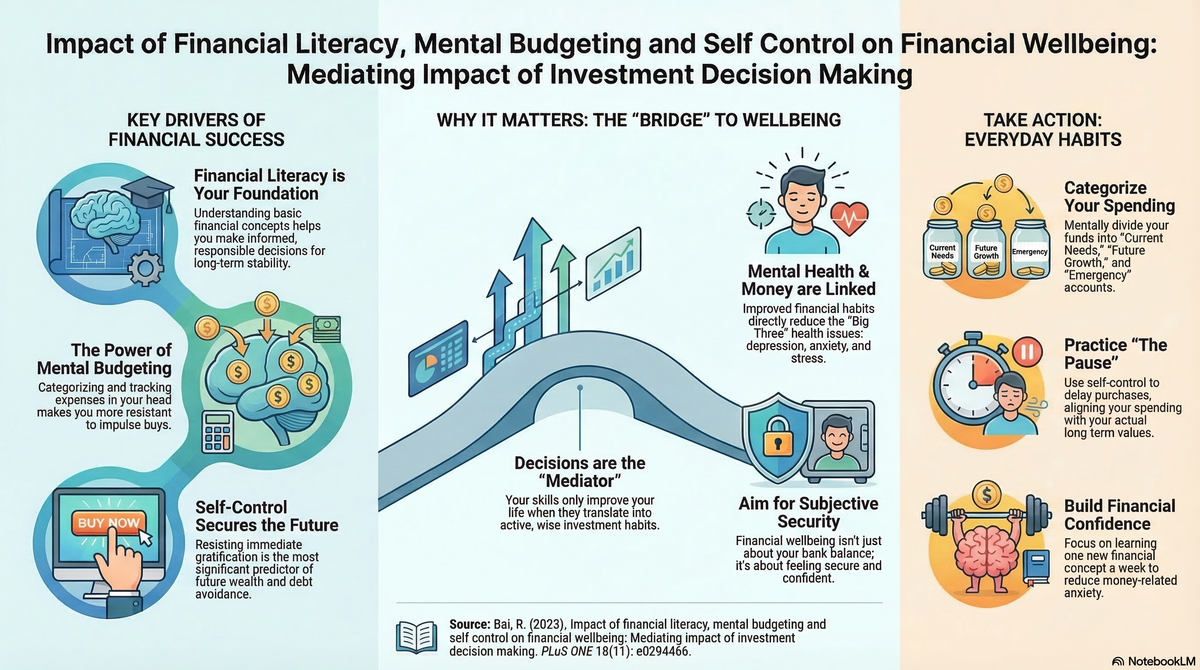

Bai, Ruofan. “Impact of Financial Literacy, Mental Budgeting and Self Control on Financial Wellbeing: Mediating Impact of Investment Decision Making.”

PLoS ONE, vol. 18, no. 11, 14 Nov. 2023, e0294466 -

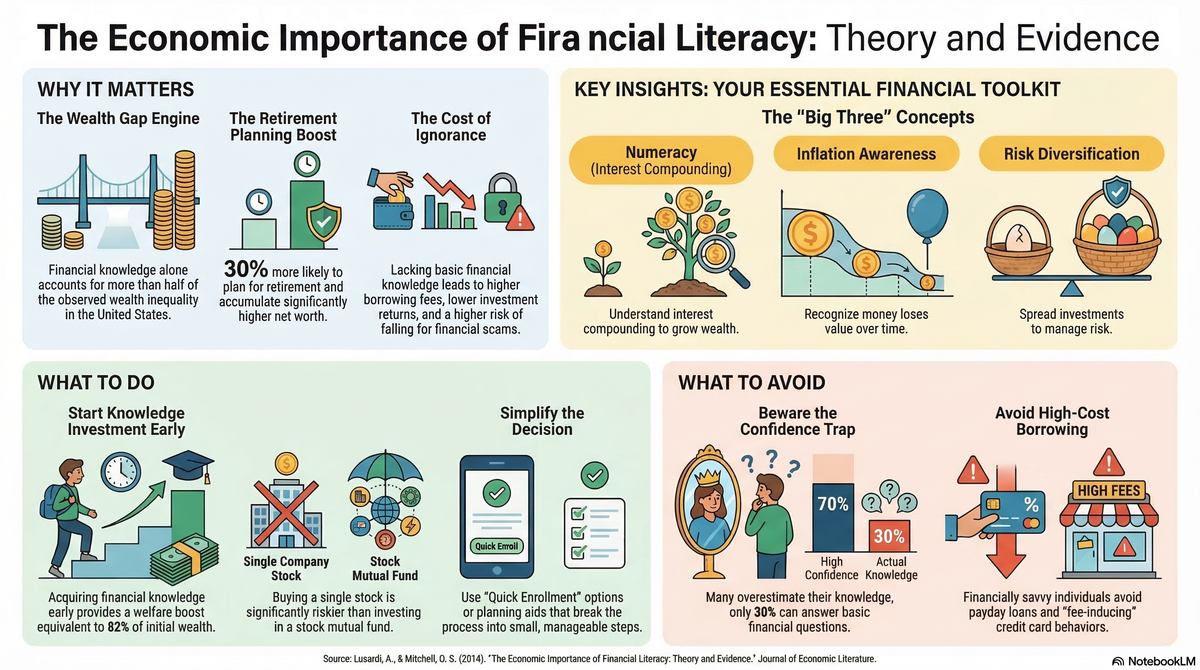

Lusardi, A., & Mitchell, O. S. The economic importance of financial literacy: Theory and evidence.

Journal of Economic Literature, 2014 52(1), 5–44