Surviving the Unexpected: What "Health financial resilience in individuals and households: a scoping review of components, strategies and outcomes" Teaches Us About Money and Well-Being

We have all experienced that sinking feeling when an unexpected bill arrives—a sudden medical emergency, a major car repair, or an unexpected loss of income. It is in these highly stressful moments that our physical health and our bank accounts violently collide. A comprehensive review exploring how people bounce back from financial shocks reveals that surviving these crises requires much more than just a lucky break or a high salary. It requires "financial resilience"—the capacity to anticipate, withstand, and recover from economic shocks without compromising your health and well-being.

Here is what the latest science tells us about building a shock-proof life and protecting yourself from the unexpected.

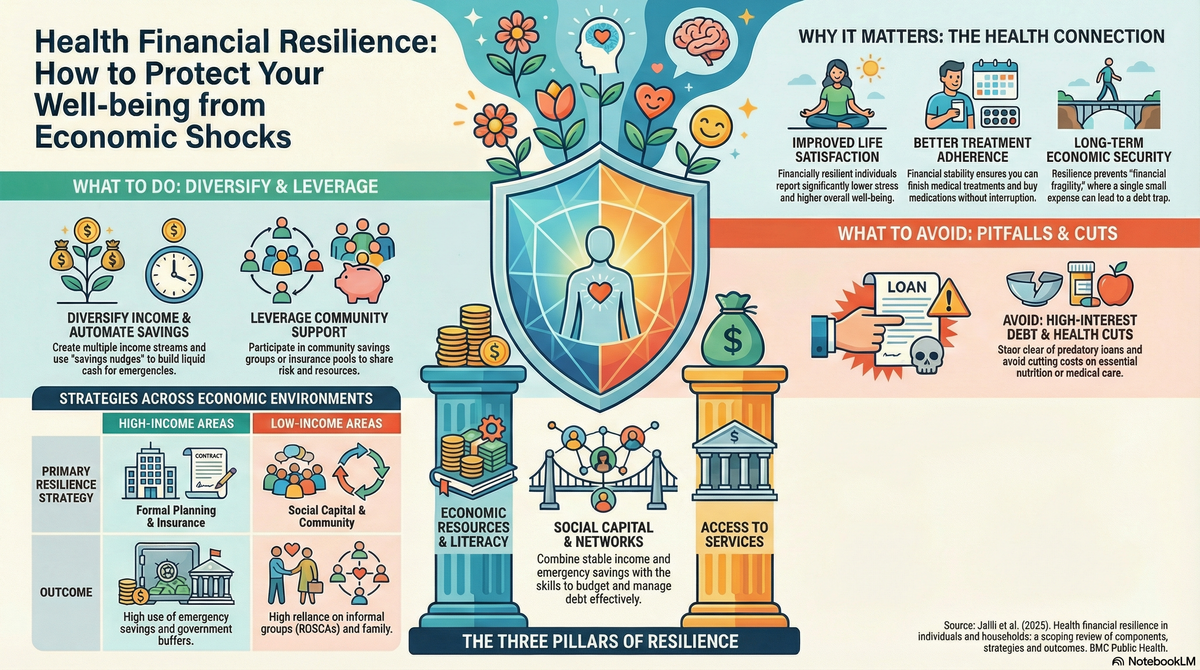

The Four Pillars of a Shock-Proof Life

Research shows that true financial resilience is a multidimensional safety net built on four core components: your economic resources (like income and savings), your financial knowledge and behavior, your social capital (your support networks), and your access to formal financial services like banking and insurance. Having a steady income alone is simply not enough if you lack the basic financial literacy to manage debt or budget effectively. To truly protect yourself, you need to cultivate all four of these pillars simultaneously.

Practical Guidance:

• What to do: Focus on building a well-rounded financial foundation by actively improving your financial literacy, such as learning how to budget, save, and invest.

• What not to do: Don't rely solely on your current paycheck to protect you; relying on income without having savings or insurance leaves you incredibly vulnerable to sudden shocks.

• Habit to change: Start educating yourself on basic financial concepts and tools rather than just letting your money sit unmanaged, so you can make informed decisions before a crisis hits.

The Art of the "Side Hustle" and Smart Savings

When disaster strikes, the most resilient households do not just panic; they lean on proactive, established strategies. One of the most effective methods for weathering a storm is income diversification, which means intentionally not relying entirely on a single paycheck. Households that combine their regular wage labor with off-farm activities, side businesses, or gig work recover much faster when one income stream dries up. Additionally, having "liquid" savings—cash that is easily and quickly accessible—acts as the ultimate shock absorber, preventing individuals from needing to sell off important assets or take out high-interest loans in a panic.

Practical Guidance:

• What to do: Build a dedicated emergency fund of liquid savings that you can access immediately without penalties or waiting periods.

• What not to do: Don't rely on high-interest, predatory loans or credit cards to fund emergencies, as these can quickly trap you in a long-term cycle of unmanageable debt.

• Decision to change: Look for ways to diversify your income, perhaps by turning a skill into a small side business, so that a single job loss doesn't completely wipe out your household's cash flow.

Your Friends Are Your Safety Net

One of the most vital insights from the research is the immense value of "social capital". In many parts of the world, especially where formal government safety nets are weak or inaccessible, people rely heavily on their community networks, family support, and informal community savings groups to survive economic crises. Having people you can trust to help you—whether through informal loans, emotional backing, or shared resources—is a legitimate, highly effective, and stress-reducing form of financial protection.

Practical Guidance:

• What to do: Cultivate strong, trusting, and reciprocal relationships within your community, family, and friend groups.

• What not to do: Don't isolate yourself when facing financial hardship; emotional and informal support from your network can be crucial for preserving your mental health and recovering your assets.

• Habit to change: Actively participate in community or family networks by offering help when you are financially stable, ensuring that the trust and reciprocity are there when you eventually need them.

The Ultimate Outcome: Protecting Your Health

Why does financial resilience matter so much? Because financial fragility directly and severely harms your physical and mental health. When people lack financial resilience, they often cope with shocks by delaying necessary medical care, skipping essential medications, or drastically cutting back on nutritious food. Conversely, those who practice financial resilience experience significantly lower financial stress, report higher overall life satisfaction, and are far better equipped to maintain their health and manage medical emergencies during crises.

Practical Guidance:

• What to do: Treat the act of building your emergency savings as a preventative healthcare measure, just like exercising regularly or eating a balanced diet.

• What not to do: Avoid coping with financial stress by cutting out essential healthcare visits or nutritious meals, as this dangerously erodes your human capital and well-being in the long run.

• Decision to change: If you are facing severe financial strain, prioritize maintaining your health coverage and seeking out community health resources before you resort to sacrificing your physical well-being to save money.

Summary for Life

The research provides a concrete life rule: Building a resilient life means treating financial literacy, emergency savings, and deep community relationships as essential, non-negotiable tools for protecting your physical and mental health from the unexpected.

Reflective Question: If your primary source of income disappeared tomorrow, do you have the liquid savings, the diversified skills, and the social network to keep your health and happiness completely intact?

References

Roya Jalili, Neda Gilani, Behzad Najafi, Vladimir Sergeevich Gordeev, and Leila Doshmangir. "Health financial resilience in individuals and households: a scoping review of components, strategies and outcomes." BMC Public Health. 2025 Sep 2;25:3021. doi: 10.1186/s12889-025-24467-5