Mastering the Money Maze: What "The Economic Importance of Financial Literacy: Theory and Evidence" Teaches Us About Wealth

Have you ever stared blankly at a retirement account enrollment form, a mortgage contract, or a credit card statement and felt totally lost? In today's world, we are increasingly expected to act as our own personal wealth managers, yet most of us were never taught how to do the job.

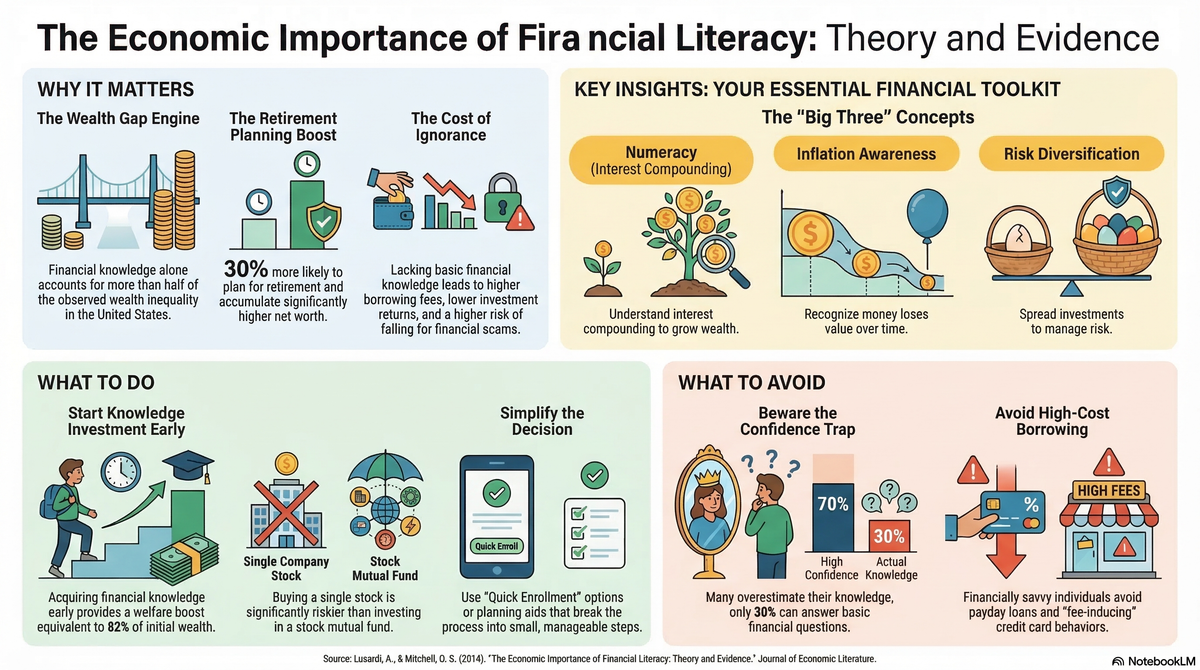

A landmark economic review explores exactly how prepared we are for this modern responsibility, and the results are eye-opening. The research reveals that understanding money isn't just an innate talent for Wall Street bankers; it is a critical life skill that directly determines our lifelong security, resilience, and wealth. Here is what the science says about the true value of financial knowledge, and how you can take control of your economic future.

The Confidence Trap

Even if you manage to pay your bills on time, you might be missing the bigger financial picture. When researchers tested adults globally on three fundamental concepts—compound interest, inflation, and risk diversification—the vast majority failed. However, the most concerning finding is not just widespread ignorance, but extreme overconfidence. Studies show that people consistently rate their own financial knowledge as very high, even when they cannot answer basic factual questions about money. This illusion of competence is dangerous because it prevents us from seeking the education or advice we desperately need, leaving us highly vulnerable to scams and poor decisions.

Practical Guidance:

- What to do: Humbly assess your actual financial knowledge by testing your understanding of core concepts like inflation, compounding interest, and how mutual funds spread risk.

- What not to do: Don't let your age or career success trick you into assuming you automatically know how to manage complex financial products.

- Habit to change: Stop pretending to understand financial jargon just to save face. Build a habit of immediately asking questions or researching terms you don't fully grasp before signing any financial document.

The "Ignorance Tax" We Pay Every Day

A lack of financial knowledge doesn't just cause anxiety; it actively drains your bank account. The research demonstrates that people with low financial literacy routinely pay a steep, invisible "ignorance tax." They are far more likely to take out costly mortgages, rack up credit card late fees, and resort to incredibly expensive borrowing methods like payday loans and auto title loans. Furthermore, they frequently miss out on significant wealth accumulation because they either avoid the stock market entirely or end up paying excessively high investment fees. Simply put, not knowing how money works is one of the most expensive mistakes you can make.

Practical Guidance:

- What to do: Calculate the true, long-term cost of your debts, especially high-interest credit cards, so you fully understand how much your borrowing is actually costing you.

- What not to do: Don't rely on high-cost, short-term borrowing (like payday loans) when you have cheaper credit available, as this is a common, costly trap for the financially uninformed.

- Decision to change: Before agreeing to any loan or investment, make a firm decision to read and understand the fee structure and the interest rate. If you cannot explain the costs to a friend, do not buy the product.

Building Your Financial "Human Capital"

We usually think of investments strictly in terms of buying stocks or real estate. But this research introduces a powerful perspective: financial knowledge is actually a form of "human capital". Just as earning a degree helps you secure a better salary, investing your time into learning about personal finance literally pays you back by helping you earn higher returns on your savings. People who invest in this specialized knowledge are significantly more likely to plan for retirement, build an emergency cushion, and ultimately accumulate much more wealth over their lifetimes. The earlier in life you build this knowledge, the longer it pays dividends.

Practical Guidance:

- What to do: Treat learning about personal finance as an active investment that requires your time and energy, just like going to the gym or learning a new career skill.

- What not to do: Don't wait until you are nearing retirement to finally figure out how your pension or savings accounts work; by then, you will have missed out on decades of growth.

- Habit to change: Shift your mindset from "I am bad with money" to "I am actively building my financial human capital." Dedicate a small amount of time each month to reading a personal finance book or taking a basic money management course.

Summary for Life

The deep truth of this economic research boils down to a single, concrete life rule: Financial literacy is not a luxury; it is a critical investment in your own human capital that protects you from costly mistakes and acts as the ultimate engine for your long-term wealth.

Reflective Question: If you treated your financial knowledge as a bank account, are you actively making deposits by learning new concepts, or is your account currently overdrawn?

References

Lusardi, A., & Mitchell, O. S. The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 2014 52(1), 5–44