Master Your Money, Master Your Mind: Understanding the "Impact of financial literacy, mental budgeting and self control on financial wellbeing: Mediating impact of investment decision making"

We have all felt the familiar knot in our stomachs when an unexpected bill arrives in the mail or when checking our bank balance near the end of the month. Financial stress is incredibly common, and it is a leading driver of depression, anxiety, and psychological distress worldwide,. When we feel like our paycheck isn't enough to cover our needs, it doesn't just empty our wallets—it drains our mental and physical health, too. We usually assume that the only cure for this stress is simply making more money.

However, a fascinating study of personal finance psychology reveals that your financial well-being is heavily dictated by how you think about money, not just how much of it you have. By mastering three specific cognitive habits, you can drastically improve your financial decisions and achieve a profound sense of security,. Here is what the science says about the psychology of wealth, and how you can rewire your brain for financial peace.

The Shield of Financial Literacy

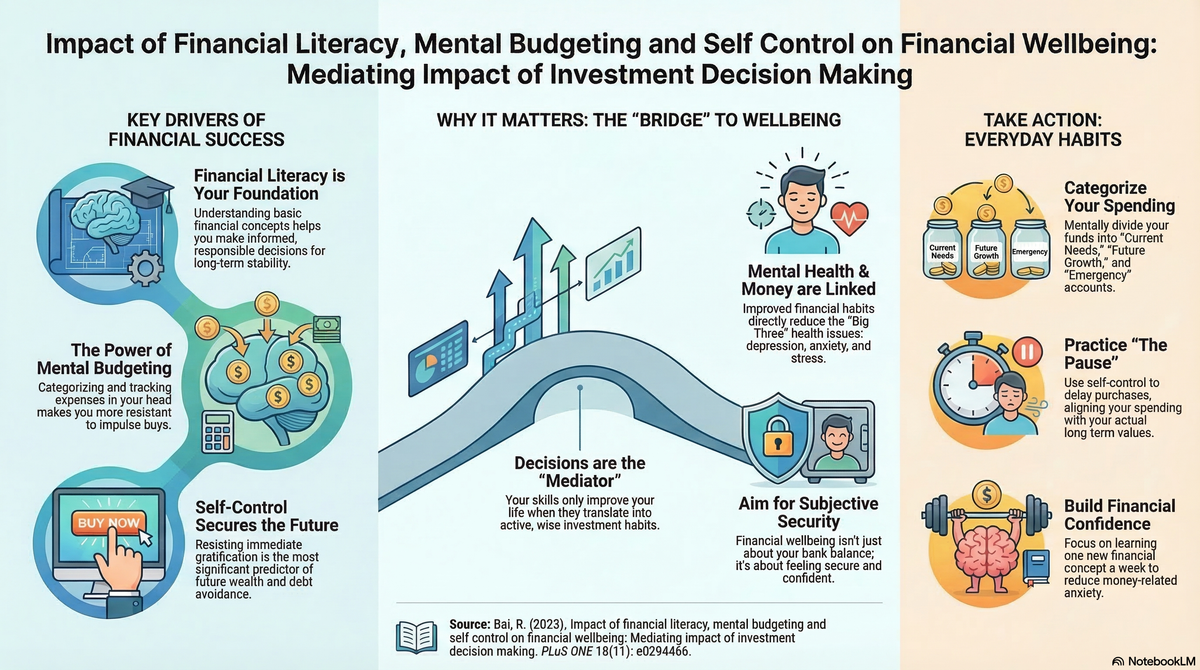

We often treat personal finance like an intimidating foreign language. But the research shows that "financial literacy"—understanding basic financial concepts and how to apply them—is one of the strongest predictors of subjective financial well-being,. Financial literacy isn't about being a Wall Street expert; it is about having the practical information and confidence required to manage your income effectively and navigate economic hazards,. When you understand how money works, you make more informed choices, which directly boosts your stability and heavily reduces your financial worries.

Practical Guidance:

- What to do: Educate yourself on the basics of personal finance. Read a beginner-friendly book or listen to a podcast about budgeting, saving, and investing.

- What not to do: Don't put your head in the sand. Ignoring your finances because they seem "too complicated" leaves you vulnerable to bad decisions and chronic stress.

- Habit to change: Dedicate just 20 minutes a week to reviewing your personal finances and learning one new money management concept.

The Magic of Mental Budgeting

You don't necessarily need a complicated spreadsheet to manage your money well. The study highlights the incredible power of "mental budgeting"—the cognitive habit of mentally classifying your income and tracking your expenditures across different categories,. People who actively mentally divide their funds into specific "buckets" (like groceries, fun money, and savings) are much more resistant to store promotions, impulse purchases, and price changes. Mental budgeting helps you maintain a firm grasp on your goals, reducing financial stress and giving you a greater sense of control over your life.

Practical Guidance:

- What to do: Mentally assign a specific purpose to every dollar you earn before you actually spend it.

- What not to do: Don't rely exclusively on credit cards without tracking your spending. Credit cards tend to blur the lines between your mental categories, making it easy to forget how much you have actually spent.

- Decision to change: Before you make a purchase, actively ask yourself which "mental folder" the money is coming from. If the folder is empty, delay the purchase.

The Power of Self-Control: Planners vs. Doers

Even the best budget will fail if you cannot resist temptation. Self-control is the ability to manage your emotions and impulses in order to achieve long-term goals. The research categorizes consumers into two mindsets: "planners," who focus on their lifetime utility and long-term goals, and "doers," who are shortsighted and seek immediate gratification. People with high self-control act as planners; they successfully avoid unnecessary debt, save more money, and invest their resources highly effectively,. Ultimately, your ability to restrict your impulsive behavior in the present defines your financial comfort in the future.

Practical Guidance:

- What to do: Establish firm saving guidelines and personal rules that automate your good decisions, making it harder to act on sudden impulses.

- What not to do: Don't sacrifice your future security for a fleeting moment of immediate satisfaction,. Avoid shopping when you are feeling highly emotional or stressed.

- Habit to change: Implement a mandatory 24-hour waiting period for any non-essential purchase. This brief pause uses your self-control to break the spell of impulse buying.

The Missing Link: Your Daily Decisions

Why do literacy, mental budgeting, and self-control matter so much? The study discovered that these three traits work together to actively improve your "investment decision-making behavior"—which is the daily process of making choices about spending, saving, and investing,. You cannot just think your way to wealth; your cognitive habits must translate into better real-world actions. When you combine financial knowledge with a mental plan and the discipline to stick to it, you naturally make smarter daily choices. These smart choices are the direct bridge to long-term financial well-being.

Practical Guidance:

- What to do: Align your daily spending choices with your ultimate, big-picture financial goals.

- What not to do: Don't view your daily purchases in isolation. Recognize that every small financial choice you make is part of your overall "investment" in your future well-being.

- Habit to change: Stop making financial decisions based purely on gut feelings or societal pressure. Filter every choice through your financial knowledge and your mental budget first.

Summary for Life

The profound truth of behavioral finance boils down to a single, concrete life rule: True financial well-being is not just determined by the size of your paycheck, but by your ability to actively cultivate financial knowledge, mentally categorize your spending, and exercise the self-control required to prioritize your future over immediate temptations.

Reflective Question: If you treated your mind as your most valuable financial asset, which cognitive habit—learning, budgeting, or self-control—would you need to invest in the most today?

References

Bai, Ruofan. “Impact of Financial Literacy, Mental Budgeting and Self Control on Financial Wellbeing: Mediating Impact of Investment Decision Making.” PLoS ONE, vol. 18, no. 11, 14 Nov. 2023, e0294466