Financial Security as the Base Layer for Growth and Meaning

Imagine standing at the edge of a vast, open field. Before you lies everything you’ve ever dreamed of: meaningful work, deep relationships, creative pursuits, and the freedom to become the person you were meant to be. Yet between you and that horizon stretches a treacherous landscape of unpaid bills, mounting debt, and the constant anxiety of wondering whether next month’s rent is covered.

This is the reality for millions of people who find themselves trapped not by lack of ambition or intelligence, but by the absence of something far more fundamental: financial security.

We often speak of money as though it exists in isolation from our deeper aspirations. Financial planning gets relegated to spreadsheets and retirement calculators, treated as a necessary but uninspiring administrative task. Meanwhile, personal growth, self-actualization, and the pursuit of meaning occupy an entirely separate conversation—one filled with inspiration, possibility, and purpose.

This artificial separation costs us dearly.

Financial security is not simply about accumulating wealth or achieving a particular net worth. It is the essential platform upon which we build lives of purpose, creativity, and genuine fulfillment. When financial instability hijacks our cognitive resources, it prevents us from pursuing higher-level goals, damages our relationships, undermines our health, and keeps us locked in survival mode.

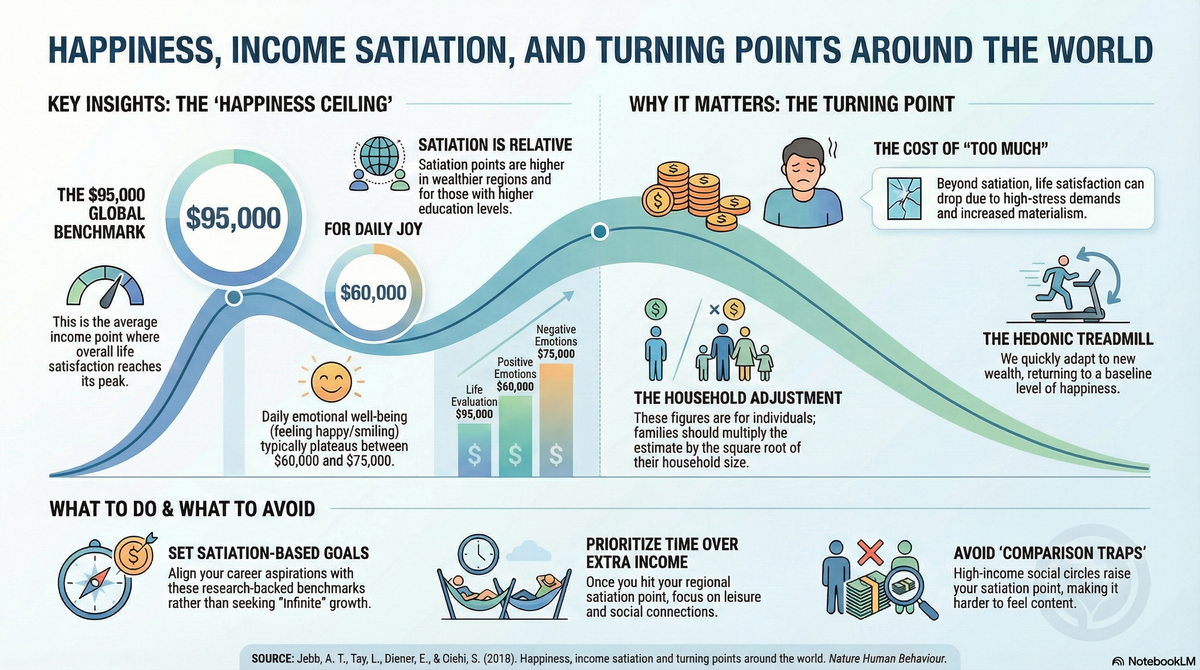

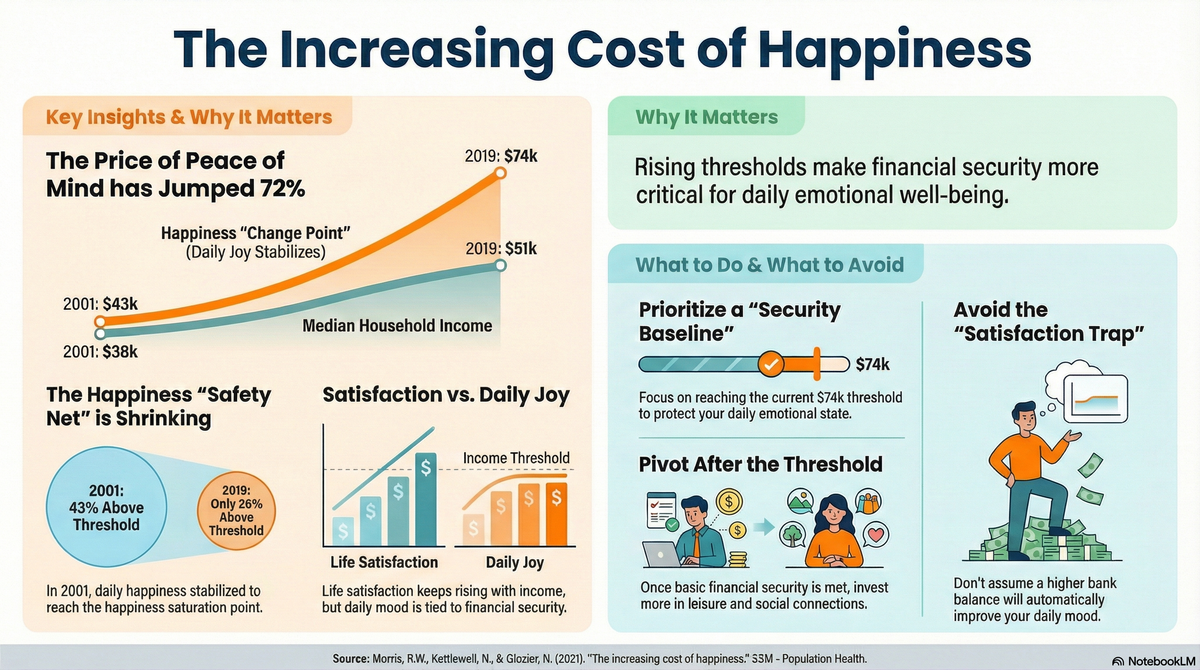

The connection between money and happiness has been studied extensively, and the research consistently reveals a crucial insight: beyond a certain threshold, additional income produces diminishing returns on well-being [1], [2]. However, beneath that threshold—when basic financial security remains elusive—the impact on every dimension of life is profound and far-reaching.

[1]

[2]

This article explores why financial security must be understood as the foundational layer for growth and meaning. We will examine the psychological frameworks that explain this connection, provide practical strategies for building your own financial foundation, and demonstrate how achieving stability in this sphere unlocks possibilities across every other area of your life.

Part 1: Understanding Financial Security

Defining True Financial Security

The term "financial security" gets tossed around frequently, often conflated with being rich, having a high income, or reaching a specific number in your bank account. These associations, while understandable, miss the essence of what financial security actually means and why it matters so profoundly for human flourishing.

True financial security is not a dollar amount. It is a state of being characterized by predictability, resilience, and peace of mind regarding your financial circumstances. Someone earning $50,000 annually with minimal debt, adequate savings, and modest lifestyle expectations may experience far greater financial security than a corporate executive earning $500,000 who lives paycheck to paycheck despite their substantial income.

Understanding the core components of genuine financial security requires moving beyond simplistic metrics like income or net worth. Instead, we must examine the structural elements that create lasting stability [3], [4]:

- Income Stability refers to having consistent and reliable income streams that you can depend upon month after month. This doesn't necessarily mean employment at a single company for thirty years—an increasingly rare arrangement in today's economy. Rather, income stability can come from diversified sources: a primary job supplemented by freelance work, investment dividends, rental income, or a side business. The key factor is predictability. When you know with reasonable certainty what money will be coming in, you can plan accordingly and reduce the anxiety associated with financial uncertainty.

[3]

- Emergency Reserves constitute the second pillar of financial security. Life is inherently unpredictable. Cars break down, medical emergencies arise, jobs disappear, and roofs develop leaks at the most inconvenient moments. An emergency fund—typically recommended at three to six months of essential expenses—provides a buffer against these inevitable disruptions. This cash cushion transforms potentially catastrophic events into manageable inconveniences. Without it, a single unexpected expense can cascade into a financial crisis, forcing people into high-interest debt that takes years to escape.

- Predictability encompasses your ability to forecast and plan for future expenses with reasonable accuracy. This involves understanding your spending patterns, anticipating upcoming costs (annual insurance premiums, holiday expenses, vehicle maintenance), and having systems in place to manage irregular but foreseeable expenses. Predictability allows you to make informed decisions about major life choices—whether to buy a home, have children, change careers, or pursue additional education—because you understand how those choices fit into your overall financial picture.

- Low Debt Burden represents another crucial element often overlooked in discussions of financial security. Debt, particularly high-interest consumer debt, creates ongoing obligations that reduce your financial flexibility and increase vulnerability to economic shocks. Financial freedom grows not just from what you earn or save, but from minimizing the claims others have on your future income.

[4]

- Appropriate Insurance Coverage provides protection against catastrophic losses that could otherwise devastate your financial position. Health insurance, disability insurance, life insurance (if others depend on your income), and property insurance create a safety net that prevents worst-case scenarios from destroying years of careful wealth-building.

When these elements work together, they create something more valuable than any specific dollar amount: financial resilience. This resilience means you can weather storms without capsizing, adapt to changing circumstances without panic, and make decisions from a position of strength rather than desperation.

Why Financial Security is a Fundamental Human Need

Financial security isn't merely a nice-to-have lifestyle upgrade. It addresses fundamental human needs that have been recognized across multiple psychological frameworks. Understanding these connections helps explain why financial instability creates such profound distress and why achieving stability unlocks potential across every dimension of human experience.

Maslow's Hierarchy of Needs

Abraham Maslow's hierarchy of needs, first published in 1943, remains one of the most influential frameworks for understanding human motivation. Maslow proposed that human needs exist in a hierarchical structure, with more basic needs requiring satisfaction before higher-level needs become primary motivators.

At the base of Maslow's pyramid sit physiological needs: food, water, shelter, sleep, and other biological requirements for survival. The second level encompasses safety needs: security, stability, protection from harm, and freedom from fear. Financial security directly corresponds to these foundational layers.

In modern society, money is the primary mechanism through which we meet physiological needs. We don't grow our own food or build our own shelter—we earn money and exchange it for these necessities. Similarly, safety needs in contemporary life are largely addressed through financial resources: secure housing, health insurance, savings that protect against unemployment, and retirement funds that ensure our old age won't be characterized by poverty.

Without adequate financial resources to address these base-layer needs, Maslow's framework suggests it becomes nearly impossible to focus sustained attention on higher-level needs. The third level—love and belonging—suffers when financial stress strains relationships. The fourth level—esteem needs—remains unfulfilled when you cannot achieve competence and independence in managing your affairs. And the pinnacle—self-actualization—remains a distant dream when daily survival demands all available energy and attention.

This doesn't mean people struggling financially never experience love, achievement, or moments of transcendence. Humans are remarkably resilient and complex. However, the consistent, sustained pursuit of higher-level fulfillment requires a foundation that financial security provides.

When you're worried about making rent, your capacity to explore creative passions, invest in personal growth, or contemplate life's deeper meanings is severely constrained.

The PERMA Model

Martin Seligman's PERMA model, a cornerstone of positive psychology, identifies five elements that contribute to human flourishing: Positive Emotions, Engagement, Relationships, Meaning, and Accomplishment. Financial security intersects meaningfully with several of these elements, particularly Engagement and Accomplishment [5].

Engagement refers to experiencing flow states—periods of deep absorption in activities that challenge and fulfill us. Financial stress is fundamentally incompatible with flow states. When your mind is occupied with financial worries, achieving the focused concentration that flow requires becomes nearly impossible. Financial security clears the mental space necessary for deep engagement with work, hobbies, and relationships.

Accomplishment involves pursuing and achieving goals, experiencing competence, and making progress toward objectives that matter to you. Financial stability enables accomplishment in two ways. First, it provides resources to pursue meaningful goals—whether that's education, starting a business, or developing a new skill. Second, achieving financial security is itself an accomplishment that builds confidence and demonstrates competence, creating positive momentum that spills into other life areas.

[5]

Financial stability also supports Positive Emotions by reducing anxiety and providing the security from which joy, gratitude, and contentment can emerge. It strengthens Relationships by removing one of the primary sources of interpersonal conflict. And it can contribute to Meaning by enabling you to contribute to causes you care about and live in alignment with your values.

The Wheel of Life

The Wheel of Life coaching tool divides human experience into interconnected spheres or domains, typically including categories such as Health, Career, Finances, Relationships, Personal Growth, Recreation, Physical Environment, and Family. While specific categories vary across different versions, the fundamental insight remains consistent: these life areas are deeply interconnected, and imbalance in one sphere affects all others.

Within this framework, Finance functions as a core sphere that impacts virtually every other domain. Consider the connections:

- Health suffers when you cannot afford nutritious food, adequate healthcare, gym memberships, or the time off work needed for rest and recovery.

- Career options narrow when financial pressure forces you to accept any available job rather than pursuing roles aligned with your skills and passions.

- Relationships strain under the weight of financial conflict—money problems remain among the leading causes of divorce and family dysfunction.

- Personal Growth stalls when you cannot afford education, coaching, books, or the time required for learning and development.

- Recreation disappears when every dollar must go toward survival.

- Physical Environment deteriorates when you cannot afford safe, comfortable housing in neighborhoods that support well-being. T

This interconnection explains why financial security isn't simply one concern among many. It is a foundational concern that enables or constrains progress across every other dimension of life. Viewing Finance as one slice of the wheel among equals understates its catalytic role. A more accurate metaphor might be viewing financial security as the hub from which other life spokes extend—when the hub is weak, the entire wheel wobbles.

The Psychological Toll of Financial Instability

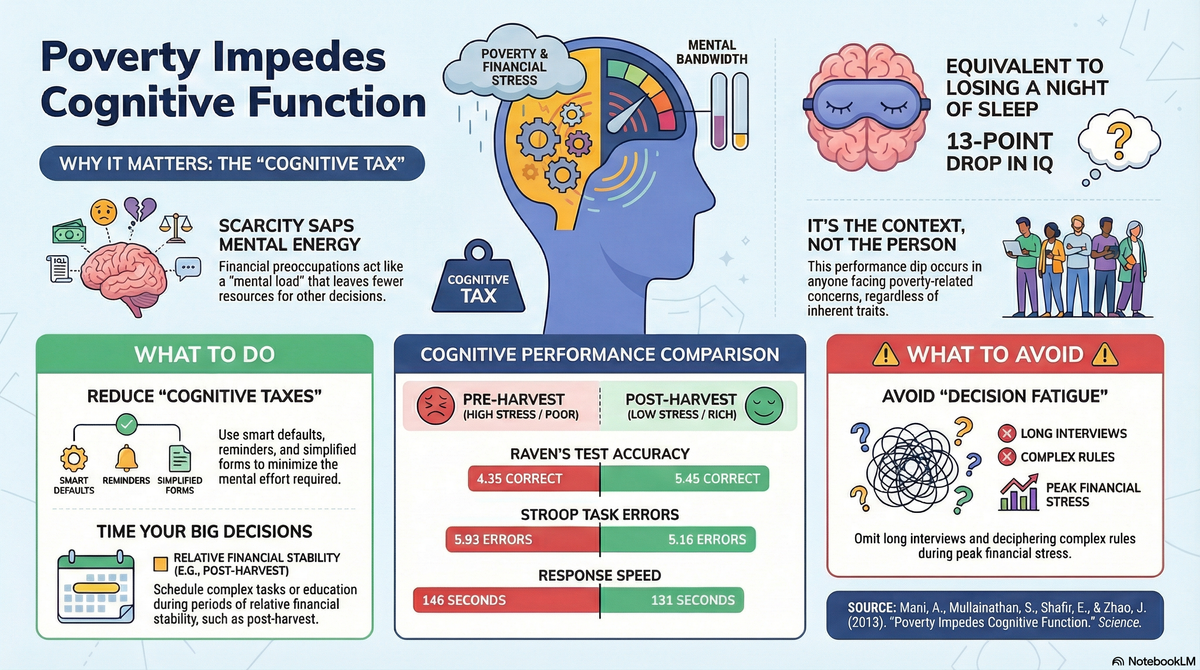

Understanding the psychological impact of financial stress reveals why achieving security is so transformative. Financial insecurity doesn't merely create worry—it fundamentally alters how our brains function, creating cognitive and emotional consequences that extend far beyond money matters [6].

Research on the psychology of financial insecurity demonstrates that it represents a major source of chronic stress. Unlike acute stress—a temporary response to an immediate threat—chronic stress persists over extended periods, creating sustained elevation of stress hormones and keeping the body in a prolonged state of physiological arousal. This chronic activation takes a measurable toll on physical health, contributing to cardiovascular disease, immune dysfunction, and accelerated aging.

[6]

The cognitive consequences may be even more significant. Financial stress impairs cognitive functions across multiple domains. Working memory—the mental workspace where we hold and manipulate information—operates with reduced capacity under financial stress. Executive functions like planning, decision-making, and impulse control become compromised. The ability to think long-term deteriorates as immediate concerns consume available mental resources.

Consider this analogy: imagine trying to run complex software on a computer with insufficient RAM. The basic programs might function, but slowly and unreliably. Attempt anything more demanding, and the system freezes, crashes, or produces errors. Your stressed brain faces a similar situation. When financial worries consume cognitive bandwidth, less processing power remains for learning new skills, focusing on complex tasks, maintaining emotional regulation, or thinking strategically about the future.

This creates a particularly cruel dynamic. The cognitive impairments caused by financial stress make it harder to escape poverty. Poor decision-making leads to choices that perpetuate financial problems. Reduced impulse control leads to spending decisions that worsen the situation. Inability to think long-term prevents the planning and delayed gratification that building financial security requires.

The result is a vicious cycle. Financial stress impairs cognitive function, which leads to poor decisions, which exacerbates financial problems, which increases stress, which further impairs cognition. This cycle explains why financial insecurity can feel so inescapable and why simply providing information about financial literacy often fails to help people in severe financial distress. The problem isn't lack of knowledge—it's lack of cognitive bandwidth to apply that knowledge effectively.

Addressing the psychological impact of financial instability is therefore as important as teaching financial skills. This means recognizing that people experiencing financial stress may need support that addresses both the emotional burden and the practical challenges. It also means understanding that achieving even modest improvements in financial security can create positive momentum—as stress decreases, cognitive function improves, enabling better decisions that further enhance security.

The mental health implications extend beyond cognition. Financial stress correlates strongly with anxiety and depression. It contributes to relationship conflict and breakdown. It affects parenting quality and childhood development. It increases substance abuse and other maladaptive coping mechanisms.

Understanding these psychological dimensions transforms how we should think about financial security. This isn't merely about having more money or achieving some arbitrary net worth milestone. It's about reclaiming cognitive resources, restoring mental health, and creating the psychological foundation from which personal growth becomes possible.

Part 2: The Path to Financial Security

The Four Levels of Financial Security

Progress toward financial security doesn't happen in a single leap. It unfolds through distinct stages, each representing a meaningful improvement in stability, freedom, and peace of mind. Understanding these levels helps you identify your current position, recognize your progress, and clarify what you're working toward. This framework describes four progressive levels of financial security:

- Survival

At the survival level, you live paycheck to paycheck. Income barely covers—or fails to cover—essential expenses. There is no buffer for unexpected costs, so any disruption (a car repair, a medical bill, a temporary reduction in hours) creates immediate crisis. Debt may be accumulating as you borrow to cover gaps between income and expenses. Psychologically, survival mode is characterized by constant stress and hyper-focus on immediate needs. Long-term planning feels impossible because you're fully occupied managing today's emergencies. Financial decisions are reactive rather than strategic—you do whatever is necessary to get through the week or month. The priority at this level is breaking the survival cycle. This typically requires some combination of increasing income (additional hours, second job, better-paying position), reducing expenses (cutting non-essential spending, finding cheaper housing, reducing food costs), and addressing any immediate crises (negotiating with creditors, seeking assistance programs, stopping the accumulation of additional debt). - Stability

At the stability level, basic needs are consistently met with a small buffer remaining. You may have a modest emergency fund—perhaps one month of expenses—and aren't accumulating new debt. You can handle minor unexpected expenses without crisis, though larger disruptions would still be challenging. This level represents a significant psychological shift. While you're not yet financially secure, you're no longer in survival mode. There's breathing room for occasional planning and the ability to think at least somewhat beyond immediate needs. The priority at this level is building resilience. This means expanding your emergency fund toward the commonly recommended three to six months of expenses, paying down high-interest debt, and beginning to think about longer-term financial goals. You may also focus on increasing income through career development, skill building, or developing additional income streams. - Freedom

Financial freedom represents a fundamental transformation in your relationship with work and money. At this level, passive income from investments, rental properties, businesses, or other sources covers your living expenses. Work becomes optional rather than mandatory—you might continue working because you find it meaningful, but you could stop without financial catastrophe. This doesn't necessarily require enormous wealth. If your annual expenses are $40,000 and your investment portfolio generates $40,000 in dividends and gains, you've achieved freedom regardless of whether that portfolio is considered "rich" by conventional standards. The math is simple: when investment returns exceed expenses, you've crossed the threshold. The psychological impact of financial freedom is profound. Decisions about work, relationships, location, and time allocation are no longer constrained by economic necessity. You can pursue work that aligns with your values rather than simply pays the bills. You can walk away from toxic situations. You can take sabbaticals, travel, or dedicate time to creative projects and personal growth. - Strategic Capital

Beyond basic financial freedom lies a level where you possess resources sufficient to make significant life choices and investments. This might include funding a business venture, making substantial charitable contributions, investing in real estate or other major assets, helping family members with significant needs, or pursuing ambitious projects that require capital. At this level, money becomes a tool for creating impact rather than simply sustaining lifestyle. The psychological experience shifts from security to empowerment—you have meaningful resources to deploy toward goals and values that matter to you. Not everyone aspires to this level, and there's nothing wrong with achieving freedom and remaining there. However, for those with entrepreneurial ambitions, philanthropic goals, or desires to leave significant legacies, strategic capital represents the final phase of financial development.

Understanding these levels serves several purposes. It helps you identify where you currently stand and celebrate progress you've made. It clarifies what you're working toward, making abstract goals concrete. It reveals that financial security is a spectrum rather than a binary state—you're always somewhere on this continuum, and every step forward matters.

Common Misconceptions: High Income vs. Real Security

Perhaps no misconception about money proves more dangerous than the belief that high income automatically produces financial security. This confusion traps countless people in cycles of financial fragility despite earning substantial salaries.

The relationship between income and security is weaker than most people assume. True security comes from a strong financial foundation—emergency fund, low debt, consistent savings, appropriate insurance—rather than from a high salary alone.

An Illustrative Contrast

Consider this illustrative scenario:

James earns $250,000 annually as a corporate attorney at a prestigious firm. From the outside, his financial situation appears enviable. He lives in an upscale neighborhood, drives a luxury car, sends his children to private school, and takes impressive vacations. His lifestyle signals success and suggests robust financial security.

In reality, James has less than one month of expenses in savings. His mortgage payment consumes over 35% of his take-home pay. His car payments, private school tuition, country club dues, and various other commitments leave him with almost nothing at month's end. If he lost his job, he would face financial crisis within weeks.

Compare James to Maria, who earns $65,000 as a high school teacher. Maria lives modestly in a small home she purchased well below what the bank approved. She drives a reliable used car, cooks most meals at home, and takes camping vacations. Her lifestyle attracts no envy or admiration.

Yet Maria has eighteen months of expenses in savings, no debt beyond her modest mortgage, and contributes 15% of her income to retirement accounts. If she lost her job, she could survive well over a year without income while finding new employment. She experiences genuine financial security that James, despite earning nearly four times as much, lacks entirely.

What explains this paradox?

The primary explanation is lifestyle inflation.

Lifestyle inflation describes the tendency to increase spending as income rises. You receive a raise and immediately upgrade your car. A promotion leads to a larger house. Growing income supports expanding expectations about what constitutes a normal or appropriate lifestyle for someone at your income level.

There's nothing inherently wrong with improving your quality of life as earnings increase. The problem arises when spending rises proportionally to income—or worse, exceeds income growth—preventing the accumulation of financial reserves that create actual security.

Lifestyle inflation often operates unconsciously. You don't deliberately decide to remain financially fragile. Instead, each incremental spending increase seems reasonable in isolation. The nicer apartment is only $300 more per month. The newer car payment fits within your budget. The upgrade from economy to business class feels like an earned reward for hard work. Individually, each choice seems sensible; cumulatively, they consume your entire income increase.

Related to lifestyle inflation is the phenomenon of "golden handcuffs"—a situation where high compensation from your current job creates dependency that makes leaving feel impossible.

Your expensive lifestyle requires your substantial salary, so you feel trapped in a position you might otherwise leave. The very income that should provide freedom instead creates imprisonment. Golden handcuffs are particularly insidious because they're self-imposed. You could, in theory, reduce expenses and regain flexibility. But the lifestyle you've built—and often the identity you've constructed around that lifestyle—makes such reduction feel unthinkable.

You're trapped not by external constraints but by your own choices and the difficulty of unwinding them. Breaking free from these patterns requires conscious attention to the distinction between income and security.

Some practical principles help:

- The gap matters more than the gross. Financial security comes not from how much you earn but from the gap between earnings and spending. Someone who earns $50,000 and spends $35,000 is building security faster than someone who earns $150,000 and spends $145,000.

- Define "enough" before lifestyle inflation takes hold. Intentionally decide what lifestyle level meets your genuine needs and contributes to your happiness. Increases beyond that point can be directed toward building security rather than expanding spending.

- Treat raises as saving opportunities first. When income increases, direct the additional funds to savings and investment before adjusting lifestyle. If you were living on your previous salary, you can continue doing so while the raise builds your financial foundation.

- Recognize that security provides more happiness than consumption. Research consistently shows that beyond a certain point, additional spending produces minimal additional happiness. Security, autonomy, and freedom from financial worry contribute more to well-being than marginal lifestyle upgrades.

The Core Financial Stack: A Practical Framework

Understanding the importance of financial security is necessary but insufficient. You also need a practical framework for building it. The Core Financial Stack breaks financial planning into four manageable layers, each essential to long-term stability and growth. Think of these layers as building blocks that must be established in roughly sequential order. Attempting to invest aggressively before establishing protection, for example, leaves you vulnerable to catastrophic setbacks that could erase your progress. Building systematically through these layers creates genuine, resilient financial security.

- Layer 1: Protection

Protection forms the base of your financial stack. This layer consists of insurance products that guard against catastrophic losses—events that could otherwise devastate your financial position and take years or decades to recover from. Essential protection includes health insurance, disability insurance, life insurance if others depend on your income, and property and casualty insurance. Protection seems less exciting than investing or wealth building. However, these protections are foundational because a single uninsured catastrophe can destroy years of careful financial progress. - Layer 2: Cash Flow

Cash flow management ensures more money comes in than goes out—the fundamental requirement for building financial security. Without positive cash flow, no other financial strategy can succeed. With consistent positive cash flow, almost any financial goal becomes achievable given sufficient time. Effective cash flow management involves tracking income and expenses, creating a spending plan, identifying and eliminating waste, and increasing income. The goal at this layer is creating consistent surplus—money remaining after all expenses that can be directed toward building security and wealth. - Layer 3: Investments

Once protection is in place and positive cash flow is established, investments grow your capital for long-term goals. This layer transforms current surplus into future wealth through the power of compound returns. Investment considerations include retirement accounts, diversified portfolio construction, consistent contribution, and appropriate asset allocation. Investing introduces complexity that the previous layers lack. However, the fundamental principle is straightforward: direct a consistent portion of income toward diversified, low-cost investments over long time periods. - Layer 4: Runway

Runway refers to the number of months you can survive without income. This metric provides a concrete measure of financial security that cuts through complexity. Your runway calculation is simple: divide your total liquid reserves by your monthly essential expenses. Runway benchmarks provide useful targets: 1-3 months (minimal buffer), 3-6 months (standard emergency fund), 6-12 months (enhanced security), 12-24 months (approaching financial freedom), and 24+ months (substantial security). Runway matters because it represents time—the most valuable resource when facing financial challenges.

Building these four layers systematically creates genuine, resilient financial security. Each layer supports the others: protection prevents catastrophic losses from destroying your progress; positive cash flow generates the surplus that builds investments and runway; investments grow wealth that extends runway and eventually generates income; extended runway provides flexibility that protects cash flow and enables strategic decisions about all other layers.

Part 3: Building a Life on a Solid Foundation

The Link Between Financial Stability and Personal Growth

With the mechanics of building financial security established, we can now explore what that security enables. The connection between financial stability and personal growth is direct and powerful—addressing base-layer needs frees mental and material resources for self-actualization and the pursuit of meaning. Recall Maslow's hierarchy: when physiological and safety needs are unmet, they consume available attention and energy. Only as these foundational needs are satisfied does sustained focus on higher-level needs become possible. Financial security directly addresses these foundational layers, creating the platform from which growth can launch. The practical mechanisms connecting financial stability to personal growth include:

- Mental space for learning and creativity. When financial stress no longer consumes cognitive bandwidth, your mind has capacity for complex learning, creative thinking, and deep engagement with challenging material. The constant background hum of financial worry quiets, allowing concentration and flow states that were previously impossible.

- Resources for education and development. Personal growth often requires investment—courses, coaching, books, workshops, conferences, degrees, certifications. Financial security provides resources to make these investments. It also provides time, perhaps the most valuable resource, to engage in learning that doesn't provide immediate income.

- Freedom to experiment and fail. Growth requires risk. Trying new things means accepting the possibility of failure. Financial security provides a safety net that makes experimentation possible. You can take on a challenging project, start a side business, or explore a new field knowing that failure won't be catastrophic.

- Capacity for long-term thinking. Self-actualization unfolds over years and decades, not days and weeks. Pursuing meaningful personal growth requires the ability to make decisions with long time horizons—accepting short-term costs for long-term benefits. Financial security enables this long-term perspective by removing the pressure to optimize exclusively for immediate needs.

- Psychological foundation for pursuing meaning. Viktor Frankl and other existential thinkers emphasized that humans are fundamentally meaning-seeking creatures. However, the search for meaning requires psychological bandwidth that survival mode doesn't provide. Financial security creates the mental and emotional foundation from which existential questions can be genuinely explored.

Consider the difference financial stability makes for someone interested in learning a new skill—say, programming. Without financial security, learning must fit around work obligations, cannot require expensive courses or equipment, and must promise relatively quick financial return to justify the investment. With financial security, learning can involve dedicated time, quality instruction, and extended periods of practice before mastery produces income. The second scenario is far more likely to result in genuine skill acquisition. This connection explains why financial security isn't separate from personal development but rather foundational to it. The common framing that positions money concerns as materialistic and growth concerns as spiritual creates a false dichotomy. In reality, addressing material needs is often the prerequisite for sustained spiritual, creative, and personal development.

Reshaping Your Career and Taking Smart Risks

Financial stability fundamentally transforms your relationship with work and your capacity to shape your career strategically. This transformation operates through several powerful mechanisms that together create unprecedented professional freedom.

- Negotiation leverage. When you need this particular job to pay next month's rent, you negotiate from weakness. When you have substantial runway and genuine alternatives, you negotiate from strength. Financial stability increases your willingness to ask for what you're worth, reject inadequate offers, and advocate for yourself effectively. Employers can sense desperation, and it works against you.

- Ability to leave toxic situations. Many people remain in jobs that damage their health, relationships, and self-respect because they cannot afford to leave. Financial security provides the exit option that transforms workplace dynamics. Even if you never use it, knowing you could leave changes how you experience work and how you're treated.

- Strategic career planning. Without financial security, career decisions optimize for immediate income and survival. With security, you can make decisions that serve long-term development even when they involve short-term costs. You might accept a lower-paying role that provides better learning opportunities, relocate to a market with more career potential, or take time off to acquire new skills.

- Entrepreneurial opportunity. Starting a business typically involves periods of low or zero income while the venture develops. Financial security provides the runway to pursue entrepreneurship—giving a business idea time to mature without the pressure of immediate profitability that kills many ventures before they have a chance to succeed.

- Risk tolerance for high-upside moves. Career opportunities often involve risk. The exciting job at the growing startup might fail. The move to a new city might not work out. The career pivot might take longer than expected. Financial security provides the cushion that makes these calculated risks acceptable.

The cumulative effect is profound. People with financial security can pursue careers aligned with their values, develop skills that matter to them, contribute in ways they find meaningful, and create professional lives that support rather than undermine their broader life goals. People without security remain trapped in survival-oriented work that may pay bills but provides little else. This isn't about privilege or entitlement. It's about understanding that building financial security is itself an act of career investment. Every dollar saved extends your runway, increases your negotiation power, and expands your options. Financial planning and career planning are not separate activities—they're deeply interconnected dimensions of building a life you want to live.

Integrating Financial Security into Your Life Plan

Financial security doesn't exist in isolation. Its effects ripple across every dimension of human experience. Understanding these connections reveals why treating Finance as just one concern among many understates its foundational importance. The VitaWell framework, which examines life across eight interconnected spheres, illustrates these connections clearly:

- Finance and Health. Financial security directly impacts health outcomes through multiple pathways: ability to afford nutritious food, access to quality healthcare, gym memberships, reduced chronic stress, time for exercise, and better living environments.

- Finance and Relationships. Financial problems are among the leading causes of relationship conflict. Financial security removes a major source of strain and enables relationship-building activities. Perhaps most importantly, it creates the emotional bandwidth for presence and connection that stress otherwise consumes.

- Finance and Career. As discussed above, financial security transforms career possibilities—enabling risk-taking, providing negotiation leverage, supporting strategic development, and allowing pursuit of meaningful work rather than mere survival.

- Finance and Personal Growth. Financial resources enable investment in education, coaching, and learning opportunities. Financial security provides time for growth activities and reduces the stress that impairs learning.

- Finance and Recreation. Leisure and recreation contribute significantly to well-being, but many activities require financial resources: travel, hobbies, entertainment. Financial security makes these restorative activities accessible and allows for spending without guilt.

- Finance and Rest. Financial security enables adequate rest through the ability to take time off, freedom from second jobs, reduced anxiety that interferes with sleep, and comfortable living conditions that support recovery.

- Finance and Physical Environment. Financial security enables safe, comfortable housing in neighborhoods that support flourishing, with adequate space and choice of location based on preferences rather than merely cost.

- Finance and Purpose/Meaning. Financial security connects to the search for meaning by providing resources for charitable giving, creating time for reflection on values, and enabling the pursuit of a calling rather than just employment.

The Wheel of Life becomes unstable when any spoke is significantly shorter than others. Finance functions as an unusually influential spoke—weaknesses here propagate through the entire wheel. Conversely, strengthening financial security creates positive ripples across all other life dimensions. This integration has practical implications for how you approach financial planning. Rather than viewing it as a separate administrative concern, understand it as foundational life planning that enables everything else you want to achieve. Time and energy invested in building financial security aren't diverted from your "real" life—they're invested in creating the conditions that allow your real life to flourish.

Conclusion: Your Platform for a Meaningful Life

We began by noting that financial security is often discussed in isolation from deeper human aspirations—separated from conversations about meaning, growth, and fulfillment. This separation impoverishes both discussions. Financial planning becomes sterile number-crunching divorced from human values when we forget why security matters. And aspirational discussions of personal growth become impractical fantasies when they ignore the material foundation that makes growth possible. The key insights from this exploration include:

- Financial security is not a dollar amount but a state of being. True security comes from structural elements like income consistency, emergency reserves, low debt, and proper protection.

- Financial security addresses fundamental human needs. It undergirds psychological well-being and enables higher-order flourishing, as shown by frameworks like Maslow's hierarchy.

- Financial insecurity creates cognitive and emotional damage. Chronic financial stress impairs decision-making and learning, creating vicious cycles.

- Progress toward security happens in stages: Survival, Stability, Freedom, and Strategic Capital.

- High income does not equal security. Lifestyle inflation can trap high earners in financial fragility.

- Building security requires a systematic approach: Protection, cash flow management, investing, and runway.

- Financial security enables personal growth and career transformation. It creates the mental space and practical freedom for self-actualization.

- Finance connects to every other life dimension. Strengthening financial security creates positive ripples across health, relationships, career, and meaning.

These insights point toward a different way of thinking about money and life planning. Financial planning isn't a restrictive chore or a necessary evil. It's not about deprivation, budgets that constrain joy, or obsessive focus on net worth.

Rather, financial planning is the ultimate act of self-care. It's the work of building the platform from which a meaningful life becomes possible.

Every dollar saved extends your runway and expands your options. Every debt paid down removes a claim on your future freedom. Every investment made compounds not just financially but in the life possibilities it creates.

The path isn't about earning as much as possible or accumulating wealth for its own sake. It's about intentionally building the financial foundation that allows you to pursue work that matters, relationships that nourish, growth that fulfills, and contributions that create meaning.

You likely already know what you would do if financial pressure weren't a constant concern. What skills you would develop. What relationships you would invest in. What creative projects you would pursue. What contribution you would make. Financial security is what makes that life possible. Not someday in a distant retirement future, but progressively, as each increment of security creates new capacity for living well.

The invitation, then, is to view your financial work—budgeting, saving, investing, career development—through this lens. You're not just managing money. You're building the foundation for a life of purpose, growth, and freedom. You're creating the platform from which meaning can emerge.

That platform starts with the next decision you make about your financial life. And the one after that. And the one after that. One choice at a time, one dollar at a time, you build the base layer for everything that matters most.

References

-

Andrew T. Jebb, Louis Tay, Ed Diener, and Shigehiro Oishi. "Happiness, income satiation and turning points around the world."

Nature Human Behaviour V2, p 33-38 (2018) -

R.W. Morris, N. Kettlewell, N. Glozier. "The increasing cost of happiness."

SSM - Population Health, vol. 16, 2021, 100949. -

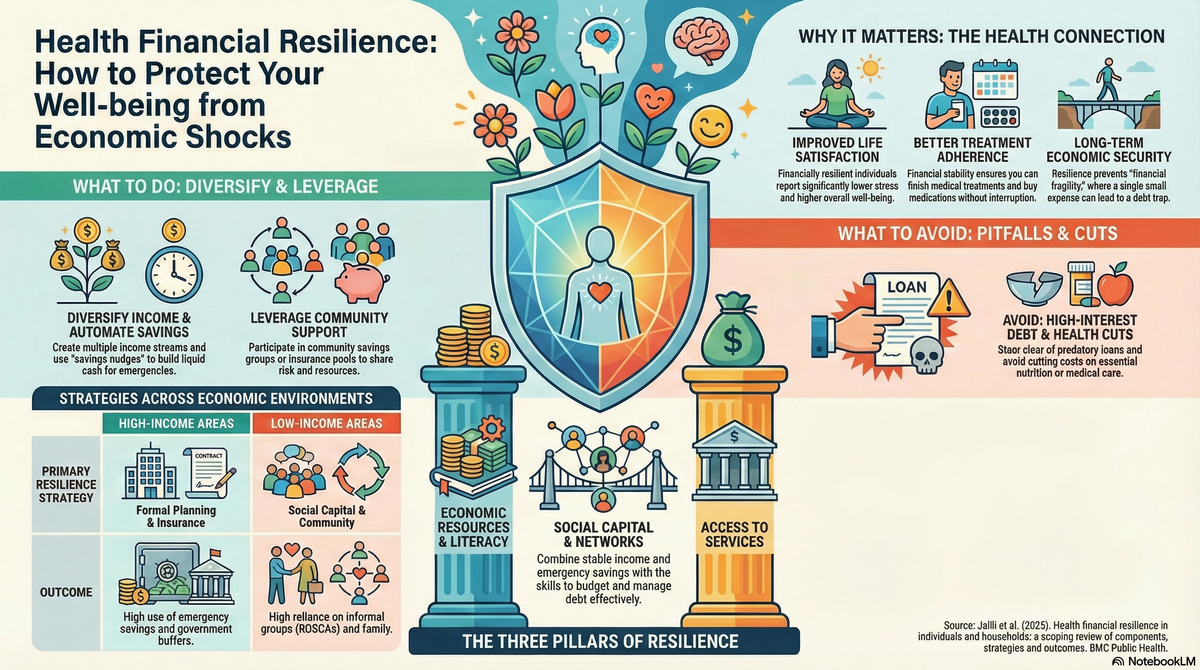

Roya Jalili, Neda Gilani, Behzad Najafi, Vladimir Sergeevich Gordeev, and Leila Doshmangir. "Health financial resilience in individuals and households: a scoping review of components, strategies and outcomes."

BMC Public Health. 2025 Sep 2;25:3021. doi: 10.1186/s12889-025-24467-5 -

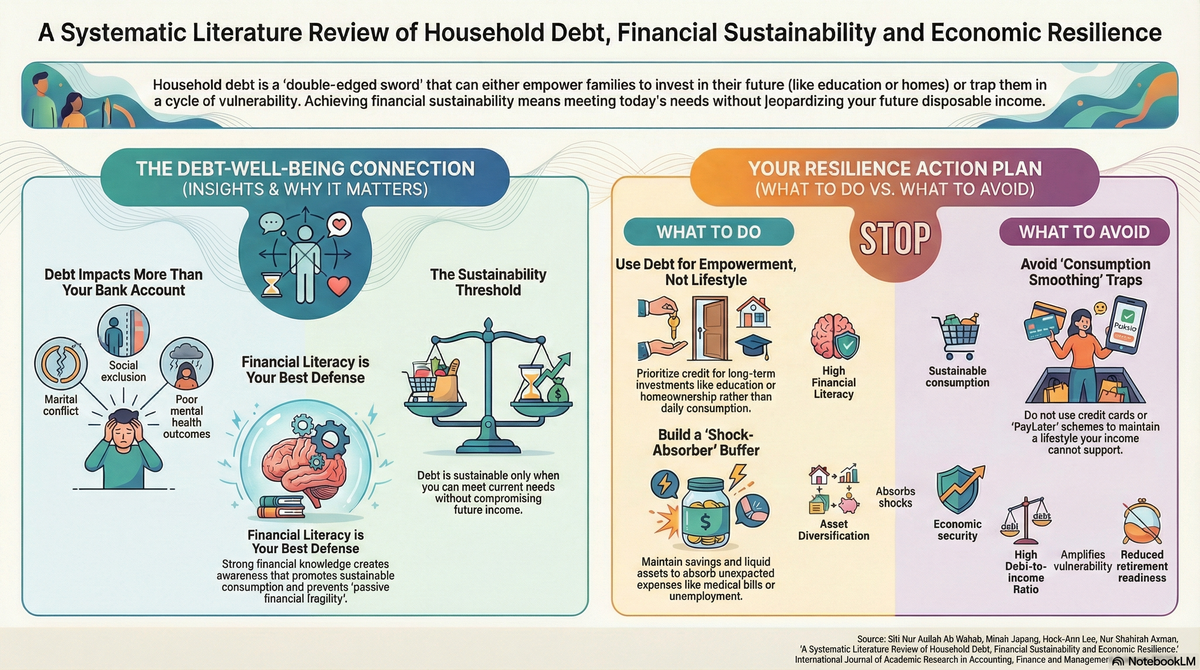

Siti Nur Aqilah Ab Wahab, Minah Japang, Hock-Ann Lee, Nur Shahirah Azman. "A Systematic Literature Review of Household Debt, Financial Sustainability and Economic Resilience."

International Journal of Academic Research in Accounting, Finance and Management Sciences, Vol. 15, No. 3, 2025. -

Maha Al-Hendawi, Ali Alodat, Suhail Al-Zoubi, and Sefa Bulut. "A PERMA model approach to well-being: a psychometric properties study.", July 2024, BMC Psychology 12(1)

DOI:10.1186/s40359-024-01909-0 -

Anandi Mani, Sendhil Mullainathan, Eldar Shafir, Jiaying Zhao. "Poverty Impedes Cognitive Function."

Science 2013 Aug 30;341(6149):976-80. doi: 10.1126/science.1238041