Breaking the Borrowing Cycle: How to Build True Wealth based on "A Systematic Literature Review of Household Debt, Financial Sustainability and Economic Resilience"

We live in a world where spending money we don't have has never been easier. From tapping a credit card for morning coffee to clicking "Buy Now, Pay Later" for a new wardrobe, borrowing has become an invisible part of our daily routines. But what happens when the convenience of credit turns into a mountain of monthly payments? A comprehensive new review of global economic research dives deep into the complex relationship between the money we owe and our long-term well-being.

This research unpacks the fine line between using debt as a helpful tool and falling into a dangerous financial trap, revealing exactly what it takes to build a shock-proof financial life.

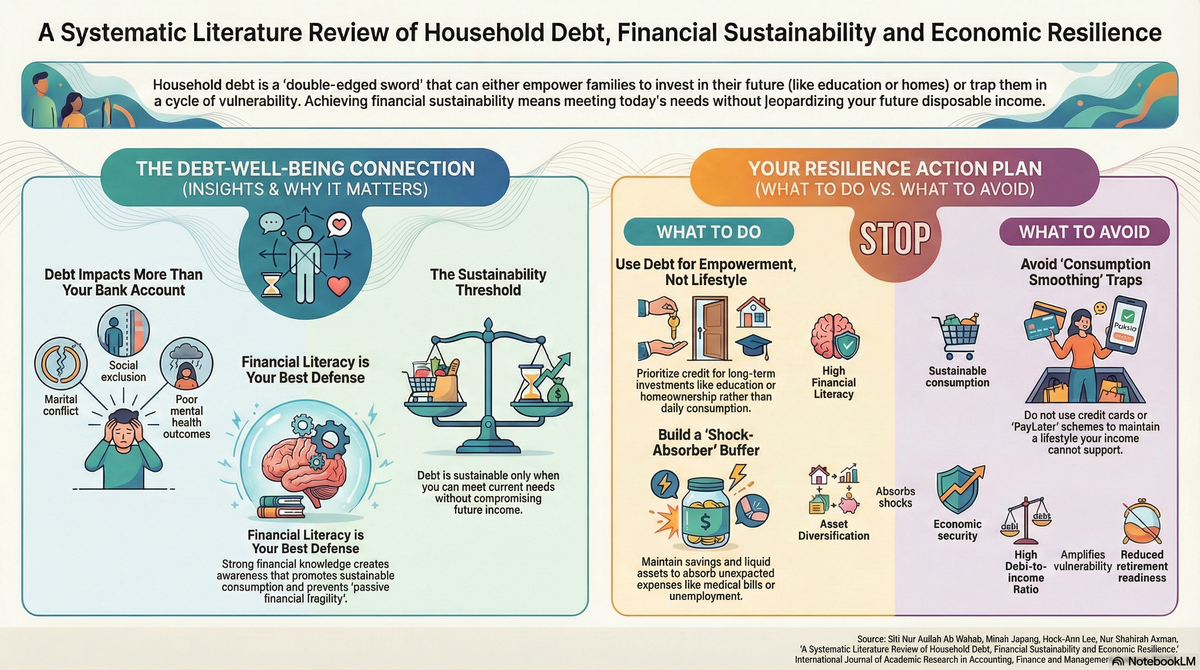

The Double-Edged Sword of Everyday Debt

Debt is often viewed simply as a necessary part of modern life. When used carefully, borrowing allows us to participate in major life milestones—like buying a home, getting an education, or starting a business. However, the research shows that debt transforms into a destabilizing force when we use it to artificially maintain our daily spending habits. When households borrow just to fund everyday consumption or mask stagnant wages, it drains their future disposable income. Over time, this "easy credit" limits your purchasing power and traps you in a cycle of endless repayment.

Practical Guidance:

• What to do: Reserve borrowing for investments that will either grow in value or increase your earning potential (like a reasonable mortgage or a degree).

• What not to do: Don't use high-interest credit cards or consumer loans to fund daily expenses, meals out, or short-term lifestyle upgrades.

• Habit to change: Audit your monthly spending to clearly separate "needs" from "wants," ensuring that your lifestyle is funded by cash you already have, not cash you hope to make tomorrow.

The Hidden Crisis of "Financial Vulnerability"

You might assume that only low-income earners struggle with financial fragility, but the research reveals a more surprising truth. Financial vulnerability is often caused by a lack of liquidity—meaning you have no easily accessible cash to handle sudden shocks like a medical emergency, a major home repair, or job loss. Even middle- and upper-income households can be incredibly fragile if all their money is tied up in heavy mortgage debt and aggressive spending. When disaster strikes a vulnerable household, it sparks a downward spiral of high-stress borrowing that has been linked to severe mental health struggles, relationship breakdowns, and social exclusion.

Practical Guidance:

• What to do: Build a dedicated, highly liquid emergency fund that can cover three to six months of basic living expenses.

• What not to do: Don't assume a high salary makes you financially secure if you are living paycheck-to-paycheck to service massive debt obligations.

• Decision to change: Treat funding your emergency savings account as a non-negotiable monthly "bill" that protects your physical and mental health.

The Trap of "Keeping Up with the Joneses"

Why do we borrow more than we should? A powerful psychological force is at play: social comparison. The research highlights that as income inequality grows, people often take on debt simply to emulate the consumption habits of their wealthier peers. This "emulation-induced borrowing" creates an illusion of wealth, but it ultimately undermines your long-term financial stability. Buying things to match a reference group provides a short-term ego boost, but leaves you with a fragile financial foundation that is highly susceptible to collapse.

Practical Guidance:

• What to do: Define your definition of success based on your actual income and personal goals, rather than external social expectations.

• What not to do: Avoid using credit to finance luxury purchases, expensive cars, or lavish vacations just to maintain a certain social image.

• Habit to change: Curate your environment. Unfollowing "luxury lifestyle" influencers on social media or stepping back from high-spending social circles can dramatically reduce the pressure to borrow.

Financial Literacy is Your Ultimate Shield

A major root cause of devastating debt traps is a simple lack of basic financial knowledge. The research confirms that individuals who lack financial literacy are far more likely to struggle with debt management, fall behind on retirement planning, and make poor investment choices. Conversely, improving your financial literacy empowers you to make proactive, informed decisions that balance your current desires with your future obligations. True economic resilience comes from understanding how money works, allowing you to adapt and recover from disruptions without your life falling apart.

Practical Guidance:

• What to do: Take active ownership of your financial education by learning how interest compounds, how to structure a budget, and how to manage debt efficiently.

• What not to do: Don't leave your financial future up to chance or rely completely on the government or banks to bail you out of poor credit decisions.

• Habit to change: Dedicate just one hour a week to your financial education—whether that means reading a personal finance book, listening to a money management podcast, or reviewing your household budget.

Summary for Life

The research leads to a concrete life rule: To achieve true financial sustainability, you must treat debt as a rare, strategic tool rather than a lifestyle crutch, protecting your peace of mind with robust cash savings and continuous financial education.

Reflective Question: If your main source of income disappeared tomorrow morning, would your current level of debt act as a minor speed bump, or would it trigger a devastating financial crash?

References

Siti Nur Aqilah Ab Wahab, Minah Japang, Hock-Ann Lee, Nur Shahirah Azman. "A Systematic Literature Review of Household Debt, Financial Sustainability and Economic Resilience." International Journal of Academic Research in Accounting, Finance and Management Sciences, Vol. 15, No. 3, 2025.